Occasionally, people tell me they’re planning to move but want to keep their house as a rental. I love the idea of owning rentals in Johnson County, KS. Rentals were my introduction to real estate. But not every house makes a good rental, and not everyone is suited to be a landlord. If you’re considering renting out your house, here are some reasons why this might not be your best option.

Should I Rent Out My House?

Many people are intrigued by the idea of owning rental properties. As mentioned, my introduction to real estate was owning and managing rentals. However, selecting the right rental property is much different than choosing to rent a house just because you happen to own it already. Not all houses make great rentals. For example, starter homes in good areas often work well, while higher end homes typically don’t generate positive cash flow. This means writing a check each month to cover the mortgage and repairs; let alone saving cash for big ticket items like a roof or HVAC system.

Inherited the house? Getting one with an existing tenant is one thing. But renting out a sentimental family home often leads to grief when tenants cause extra wear and tear. I often see people renting out inherited homes to struggling family members. Those folks are usually in tough spots for good reasons. Helping family is admirable, but be brutally honest about sustainability. There’s a big difference between helping and enabling.

Underwater, but moving? Another common reason people want to convert their house into a rental is when they plan to move but the house is underwater (owing more than the house is worth). If that’s you, I’d strongly consider your reasons for moving. If you have the choice staying put and keeping the house if often a better solution.

If you’re moving out of state and the house is underwater, you might be facing a foreclosure or short sale. Either one will destroy your credit. Believe it or not, putting a tenant in your house can actually throw fuel on the fire. That’s because, you really need cash reserves to own a rental (more on the “hidden” costs later). Hoping a tenant will make things better is typically just delaying the inevitable.

The “Tenants and Toilets” Reality

Owning rentals isn’t “passive income”, despite what the gurus tell you. Landlording is a business, more specifically it’s a people business. Tenants and toilets are not for everyone. When the heater stops working on Christmas Day, you owe it to your tenants to address the issue ASAP. You don’t have the luxury of dealing with issues whenever it’s convenient for you, nor should you spend weeks price shopping before addressing urgent situations. If you’ve never managed rental properties, consider hiring a property manager. They’ll find the tenants and answer the phone calls.

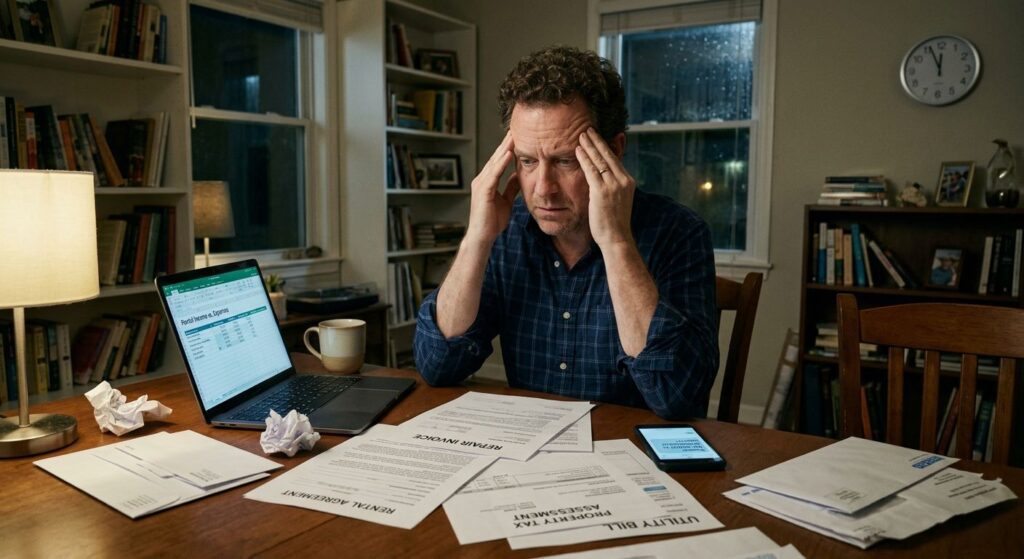

Silent Costs to Consider

The finances on a rental property aren’t as simple just subtracting the mortgage from the gross rental income. Most people underestimate the other costs involved. Before you decide to rent out your house, let’s talk about some of these “silent” costs.

- Vacancy: Sometimes the property will sit vacant between tenants. That means not only loss of rent, but also added expenses such as utilities and lawn maintenance a tenant would normally cover. Even worse is the fact that empty properties are like bad luck magnets. What can go wrong, often does. I’ve seen vandalism, stolen AC units and copper piping, and even squatters.

- Maintenance and Turn-over: Things will break and you’ll pay to fix them. Paint and carpet between tenants is typically the minimum. Further, you cannot legally charge the tenants for normal wear and tear (nor should you). Even good tenants sometimes break things they have pay for, but can’t afford to right away. Do you work with them or start eviction? You need to keep the property in good shape, or tenants will subconsciously take worse care of it.

- Capital Expenditures (CapEx): Small repairs are one thing, but major items like roofs or HVAC systems can wipe out years of cash flow. It’s best to save a portion of the rent each month for CapEx. Put big ticket items in the budget.

- Landlord Insurance: A standard homeowner’s policy doesn’t cover rentals. Non-owner-occupied policies are often more expensive and have different coverage limits. Many times, you need to confirm your tenants have their own renters insurance.

- Lawsuits and Lead-Based Paint: Owning rental properties means you have to follow certain laws when choosing tenants and make certain disclosures. Otherwise, you’re likely treating people unfairly. And setting yourself up for a lawsuit. In addition to state and federal laws, cities also have their own, unique laws. In parts of the Kansas City metro, ‘Right to Counsel’ laws mean the city may provide a tenant with an eviction lawyer for free, despite who’s “at fault”. This can make the process significantly longer and more expensive for a landlord, regardless of the facts.

- Tax Implications: Converting your personal residence into a rental might mean you lose your capital gains exemption (one of the biggest tax perks of homeownership). Under IRS § 121, you generally need to have lived there at least two of the last five years to qualify when selling. This is especially important if you’ve gained a lot of equity prior to converting the property into a rental. Disclaimer: always check with your CPA when it comes to taxes.

Let’s Run The Numbers

Before you decide about renting out your house, let’s sit down and run the numbers. With nearly 20 years owning and managing rentals, I can run the real numbers with you. Then compare them to alternatives such as rolling equity into your next home or buying a property better suited as a rental. If neither of those apply, simply putting the equity into stable mutual funds can be a great option. Once you have firmer numbers, you can decide whether or not renting out your house is good plan for you.

Justin Rollheiser – Real Estate Agent

REALTOR®

Keller Williams Realty Diamond Partners, Inc.

13671 S Mur-Len St, Olathe, KS 66062

Cell 913-800-7653

Office 913-322-7500

www.JustinRollheiser.com

Comments or Questions?